Diamond News Archives

- Category: News Archives

- Hits: 1031

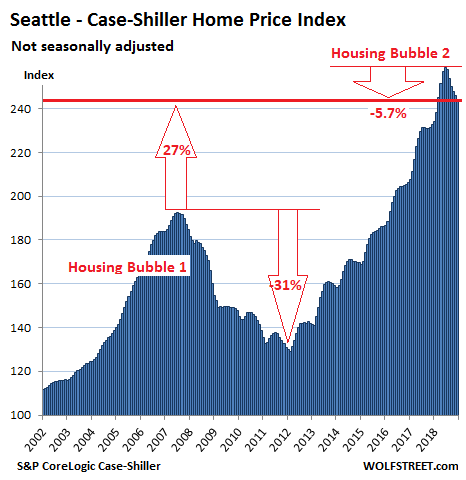

San Francisco Bay Area & Seattle lead with biggest multi-month drops since 2012; San Diego, Denver, Portland, Los Angeles decline. Others have stalled. A few eke out records.

San Francisco and San Diego are catching the Seattle cold, and others are sniffling too, as the most splendid housing bubbles in America are starting to run into reality.

House prices in the Seattle metro dropped 0.6% in December from November, according to S&P CoreLogic Case-Shiller Home Price Index[1], released this morning, and have fallen 5.7% from the peak in June 2018, the biggest six-month drop since the six-month drop that ended in February 2012 as Housing Bust 1 was bottoming out. The index is now at the lowest level since February 2018. After the breath-taking spike into June, the index is still up 5.1% year-over-year, and is 27% higher than it had been at the peak of Seattle’s Housing Bubble 1 (July 2007):

So Seattle’s Housing Bubble 2 is unwinding, but more slowly than it had inflated. Many real estate boosters simply point at the year-over-year gain to say that nothing has happened so far — which makes it a picture-perfect “orderly decline.”

San Francisco Bay Area:

The Case-Shiller index for “San Francisco” includes five counties: San Francisco, San Mateo (northern part of Silicon Valley), Alameda, Contra Costa (both part of the East Bay ), and Marin (part of the North Bay). In December, the index for single-family houses fell 1.4% from November, the steepest month-to-month drop since January 2012. The index is now down 3% from its peak in July, the biggest five-month drop since March 2012.

Given the surge in early 2018, the index is still up 3.6% from a year...

- Category: News Archives

- Hits: 957

The Swiss Gemmological Institute SSEF has announced the launch today of GemTrack™, a new service providing expert scientific opinion linking a cut gemstone to the rough stone from which it originated, thus enabling gemmologically the documentation of part of the stone's journey from mine to market.

The GemTrack™ service involves the combination of crystallographic, structural, chemical and microscopic analyses, which allow for a detailed and potentially unique characterisation and fingerprinting of a rough stone. These same features can later be later be identified during the investigation of a resultant cut stone, following the cutting and polishing process, and documented on a GemTrack™ report.

A GemTrack™ document may also be issued if a gem is later mounted in jewellery, in order to document the stone all the way from the rough state to an item of jewellery.

A GemTrack™ report will not make any specific claims of mine of origin. However, when credible documentation is provided (such as transparent sales receipts from a rough auction), it may state that, based on provided documentation, a gemstone was sourced from a specific company or auction.

...

- Category: News Archives

- Hits: 1026

Botswana has offered to lend Zimbabwe $600 million to support its diamond industry and local private firms, a state-owned newspaper reported on Tuesday, amid a severe dollar crunch in the southern African nation.

There are few signs the flow of foreign currency is improving in Zimbabwe after it ditched a discredited 1:1 dollar peg for its dollar-surrogate bond notes and electronic dollars, merging them into a lower-value transitional currency called the RTGS dollar.

James Manzou, Zimbabwe's secretary for foreign affairs, said President Emmerson Mnangagwa and Botswana's President Mokgweetsi Masisi are expected to sign the loan agreements in Harare on Thursday.

The loan will consist of $500 million dollars for Zimbabwe's diamond industry and a further $100 million to help private companies, whose operations have been hamstrung by the dollar shortage, the state-owned Herald newspaper said.

"Zimbabwe is also appreciative of the $500 million diamond facility offered to it by Botswana," Manzou was quoted as saying by the paper.

Manzou, who could not be reached for comment, did not give any details on the diamond loan.

Last month South Africa said it had turned down Zimbabwe's request for a $1.2 billion loan.

Zimbabwe's diamond sector has struggled since the government kicked out private companies from the eastern Marange fields in early 2016 after they declined to merge under the state-owned mining company.

Relations between Zimbabwe and Botswana have improved recently following a strained period when Botswana's ex-President Ian Khama, who stepped down in 2018, routinely criticised Zimbabwe's former strongman Robert Mugabe for holding on to power for too long.

A military coup in 2017 forced Mugabe to resign, ending his 37-year rule.

(By MacDonald Dzirutwe; Editing by Kirsten Donovan)

The post Botswana offers Zimbabwe $600m of loans...

- Category: News Archives

- Hits: 1041

Unless the Fed is going to start buying millions of homes outright, prices are going to fall to what buyers can afford.

There are two generalities that can be applied to all asset bubbles:

1. Bubbles inflate for longer and reach higher levels than most pre-bubble analysts expected

2. All bubbles burst, despite mantra-like claims that "this time it's different"

The bubble burst tends to follow a symmetrical reversal of very similar time durations and magnitudes as the initial rise. If the bubble took four years to inflate and rose by X, the retrace tends to take about the same length of time and tends to retrace much or all of X.

If we look at the chart of the Case-Shiller Housing Index below, this symmetry is visible in Housing Bubble #1 which skyrocketed from 2003-2007 and burst from 2008-2012.

Housing Bubble #1 wasn't allowed to fully retrace the bubble, as the Federal Reserve lowered interest rates to near-zero in 2009 and bought $1+ trillion in sketchy mortgage-backed securities (MBS), essentially turning America's mortgage market into a branch of the central bank and federal agency guarantors of mortgages (Fannie and Freddie, VA, FHA).

These unprecedented measures stopped the bubble decline by instantly making millions of people who previously could not qualify for a privately originated mortgage qualified buyers. This vast expansion of the pool of buyers (expanded by a flood of buyers from China and other hot-money locales) drove sales and prices higher for six years (2012-2018).

As noted on the chart below, this suggests the bubble burst will likely run from 2019-2025, give or take a few quarters.

The question is: what's the likely magnitude of the decline? Scenario 1 (blue line) is a symmetrical repeat of...

- Category: News Archives

- Hits: 898

There has been a lot written recently about the forces that have led us to the current “winner-take-all” economy, or what some have called a new, “gilded age,” a reference to the time when a handful of large “trusts” dominated their respective industries. Most seem to blame the lack of antitrust enforcement and growing corporate influence in Washington and these have obviously played a role. However, there are a pair of far less obvious forces at work in the markets that may have had just as much influence in this regard.

Harvard Business Review recently tackled the topic of growing corporate concentration and anti-competitive behavior as it relates to the rise of passive investing. They demonstrate that the rapid growth of common ownership of multiple companies in the same sector has supported the rise of oligopolies and enabled anti-competitive behavior across a number of industries.

Horizontal shareholding hurts competition because it reduces “each individual firm’s incentives to cut prices or expand output by increasing the costs [to shareholders, and thus managers] of taking away sales from rivals.” https://t.co/wq9hXLCZKM pic.twitter.com/71r5bomeGn[1][2]

— Jesse Felder (@jessefelder) February 20, 2019[3]

Similarly, a new research paper finds that low interest rates, such as those enabled by the world’s major central banks over the past decade, also encourage the sort of corporate concentration that allows for anti-competitive practices.

This study provides a new theoretical result that low interest rates encourage market concentration by giving industry leaders a strategic advantage over followers, and this effect strengthens as the interest rate approaches zero. https://t.co/oKC6iVrCag cc @jtepper2[4][5]

— Jesse Felder (@jessefelder) February 18, 2019[6]

These two pieces of...