Diamond News Archives

- Category: News Archives

- Hits: 807

By John Mauldin

Here is a quote from my friend Peter Boockvar that has drawn an enormous amount of interest: “We no longer have business cycles, we have credit cycles.”

Let’s cut that small but meaty sound bite into pieces. What do we mean by “business cycle,” exactly? Well, it looks something like this.

A growing economy peaks, contracts to a trough (what we call “recession”[1]), recovers to enter prosperity, and hits a higher peak. Then the process repeats.

The economy is always in either expansion or contraction. However, this pattern broke down in the last decade.

Low Rates to Blame

In the 2008 financial crisis, we had an especially painful contraction[2]. It was followed by an extraordinarily weak expansion.

GDP growth should reach 5 percent in the recovery and prosperity phases, not the 3 percent we have seen since 2008.

Peter blames the Federal Reserve’s artificially low interest rates[3]. Here’s how he put it in one of his letters:

To me, it is a very simple message being sent. We must understand that we no longer have economic cycles. We have credit cycles that ebb and flow with monetary policy. After all, when the Fed cuts rates to extremes, its only function is to encourage the rest of us to borrow a lot of money and we seem to have been very good at that. Thus, in reverse, when rates are being raised, when liquidity rolls away, it discourages us from taking on more debt. We don’t save enough[4].

The problem is that, over time, debt stops stimulating growth[5]. Debt-fueled growth is fun at first but simply pulls forward future...

- Category: News Archives

- Hits: 901

More than three years after two treasure hunters claimed to have found a Nazi train laden with gold and gems in the Polish city of Walbrzych, one of the men looking for it has unearthed another kind of treasure: two dozen priceless Renaissance portraits.

Piotr Koper, who spent years hunting for the elusive train rumoured to be laden with gold and gems, has found two dozen priceless Renaissance portraits.

Piotr Koper made the completely accidental discovery while helping renovate a baroque dome in a palace located in the village of Struga, near the city of Wroclaw, local outlet The First News reported.

Since one of the portraits depicts Ferdinand I Habsburg, ruler of the Holy Roman Empire from 1558 till 1564, the renovators deduced that the paintings are at least 500 years old.

The owner of the palace where the portraits were found believes that there may be many other valuable objects to discover there.

Koper’s earlier obsession with the Nazi Gold Train made international headlines between 2015 and 2016.

According to tales that have circulated since the end of World War II, the Nazis hid a train containing up to 300 tons of gold, as well as diamonds and firearms.

A number of trains are believed to have been used by the Nazis in the 1940s to transport goods stolen from people in Eastern Europe back to Berlin. While some might have made it to the German capital, others are said to have been left behind by Soviet troops, as they advanced in 1945.

The post Polish looking for ‘Nazi Gold Train” finds another kind of treasure appeared first on MINING.com....

- Category: News Archives

- Hits: 954

- Category: News Archives

- Hits: 868

The Accredited Gemologists Association announced the presenters of its AGA Las Vegas Conference that will take place on Friday, May 31, 2019 at the Westin Las Vegas.

A regular at AGA conferences, GIA's Shane McClure will be talking about "Detecting Heat Treatment Levels in Corundum." McClure, a recipient of the Antonio C. Bonanno Award for Excellence in Gemology (2007), will tell how low-temperature treatments are now being detected and what to look for at each temperature range for corundum. Mozambique rubies and basaltic blue sapphires are among those being revisited with this new information.

Dr. Thomas Hainschwang, of GGTL Laboratories of Liechtenstein, also a recipient of the Antonio C. Bonanno Award for Excellence in Gemology (2015), will offer a research grant update and report on current results from a major diamond research project, funded in part by an AGA research grant. He will speak about the cause of color determination, pre and post-treatment observations and cataloging properties of some of the world's important diamonds.

...

Dror Yehuda is a a third generation diamantaire. His father, Zvi Yehuda, is a world famous scientist who introduced numerous revolutionized inventions into the diamond and jeweler industry. Dror will address synthetic diamond detection and tell participants about the development of the Sherlock Holmes Detector, a tabletop machine that quickly reveals HTHP and CVD synthetics. He will also allow attendees a hands-on opportunity with "SHERLOCK" and, in addition, provide an update on the state of clarity-enhanced diamonds and their pricing.- Category: News Archives

- Hits: 913

This post is based on excerpts from recent reports published at TFR Premium[1].

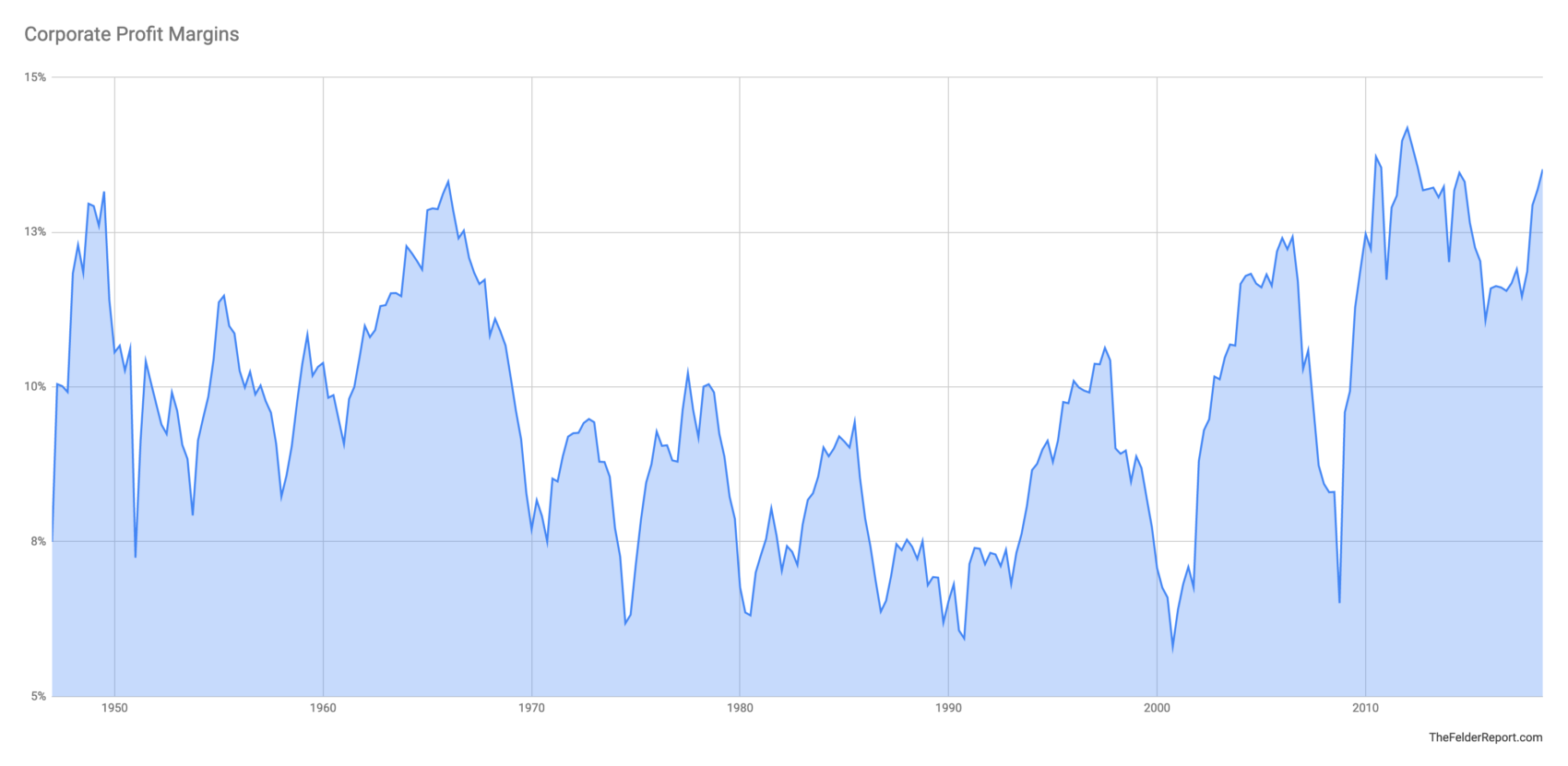

A couple of weeks ago[2], I wrote about how extreme valuations can be explained by extreme sentiment or euphoria. This week, I’d like to discuss the sort of euphoria we are witnessing in regards to owning equities today because it’s certainly very different than the sort of euphoria we saw at the peak of the dotcom mania, the last time valuations were as high as they are today. Back then, investors were making heroic assumptions about the prospects for growth in corporate sales and earnings. Today, they are making heroic assumptions about the sustainability of corporate profit margins and valuations, even if they’re not conscious of doing so.

As noted in my last post, the Buffett Yardstick is near all-time highs. However, while earnings based measures still show the stock market to be expensive they suggest the over-valuation is less extreme. The difference is the former is not affected by profit margins and the later is entirely dependent upon them. Thus investors leaning on earnings-based measures like the price-to-earnings ratio are making the assumption that margins will at least maintain at their current record highs indefinitely, as euphoric a premise as I’ve ever seen.

This issue of profit margins is so critical because if earnings-based valuations were to simply return to their historical averages it would mean a substantial decline in prices. But if profit margins were to revert at the same time, it would mean a far more substantial decline. It works like this: trailing earnings for the S&P 500 are currently $130. Put a 15x multiple on that, the long-term historical average, and you get a price of 1,950 for the index, or 30%...