“Even the most circumspect friend of the market would concede that the volume of brokers’ loans—of loans collateraled by the securities purchased on margin—is a good index of the volume of speculation.” -John Kenneth Galbraith, The Great Crash, 1929

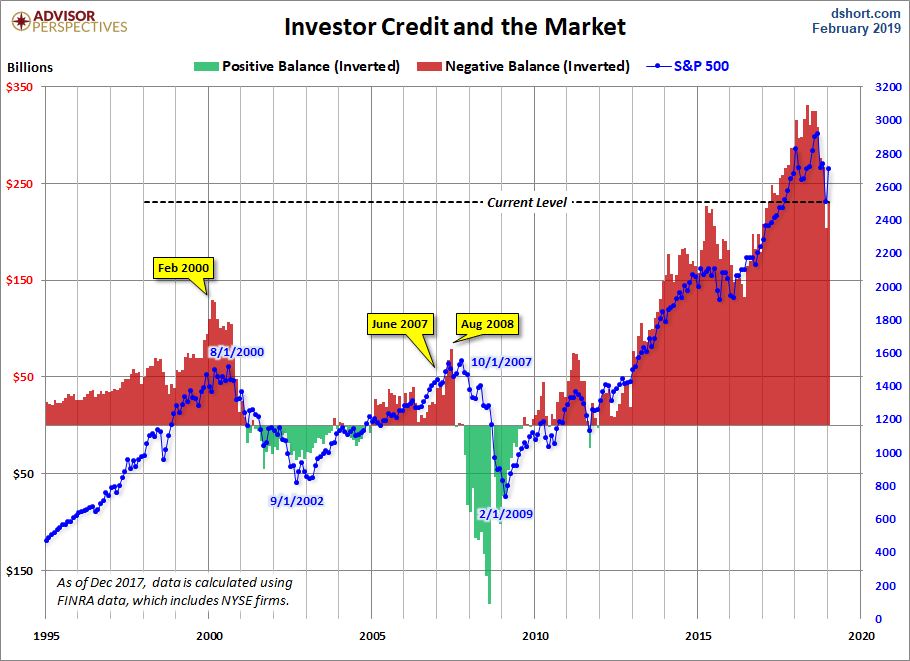

January margin debt figures were recently released (chart below via dshort.com[1]) and almost immediately prominent pundits jumped to allay the natural concerns regarding the sheer amount of leveraged speculation in the market at present. Their common refrain has been to suggest that it’s not the amount that is important but its size in relation to the overall size of the market.

This sounds reassuring on its surface but, logically, it should be entirely unconvincing. Suggesting margin debt figures should only be compared to market capitalization is akin to suggesting a smoking habit should only be compared to body weight. In this case, the larger the human being, the less risk he or she would be taking in smoking three packs a day. A patient heeding this advice would then come to the conclusion that in order to ameliorate his smoking habit he should gain as much weight as possible. Of course, this is absurd.

“In accordance with the cultural practice, as the summer passed, the sound and responsible spokesmen decried not the increase in brokers’ loans, but those who insisted on attaching significance to this trend.” -John Kenneth Galbraith, The Great Crash, 1929

Just as absurd is to suggest that well over half-a-trillion-dollars in market leverage is less dangerous than it might appear due to the fact that the market itself is so highly valued. Along this line of thinking, the greater the bubble in equity valuations, the less problematic margin debt becomes....